A kitchen full of cooks: Harmonising the carbon market

Nick Osborne, Vice President, Global Carbon and Environmental Products Trading at Shell, explains why greater alignment on standards and data quality can help the voluntary carbon market move from fragmentation toward trust and scale.

Nick Osborne, Vice President, Global Carbon and Environmental Products Trading at Shell

Nick has over 25 years of experience at Shell, with a trading career spanning since 2000 across gasoline, chemicals and related products. He led the global ethanol business from 2006 to 2012, scaling it from a single trader operation into a global team.

A fragmented ecosystem limiting trust and supply

At a BNEF London roundtable I hosted on carbon credit procurement, one participant described today’s voluntary carbon market (VCM) as “a kitchen with too many cooks.” It’s a useful analogy: the VCM is bustling with activity and a growing cast of players. Integrity bodies, standard setters, rating agencies, and intermediaries are all striving towards the same goal: to build trust, improve transparency, and define what “quality” truly means in carbon credits.

Progress is underway. Organisations such as the Integrity Council for the Voluntary Carbon Market (ICVCM) and the Voluntary Carbon Markets Integrity Initiative (VCMI) are helping to bring more consistency to integrity and claims. Meanwhile, the potential convergence of compliance markets – such as Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) and the EU Emissions Trading Scheme (ETS) – with the VCM could see compliance-grade standards influence the VCM.1

But defining quality is only part of the challenge. Translating quality standards into consistent, investable supply remains difficult. CCP-labelled credits, for example, are still emerging and availability can be limited across some project types and vintages. According to MSCI, less than 5% of credit surplus today is CCP approved (approximately 52 million tonnes), underscoring the current scarcity of high-quality supply.2

Webinar: Navigating quality in voluntary carbon markets

Nick Osborne, Vice President, Global Carbon and Environmental Products Trading at Shell, shares insights on the evolving voluntary carbon market and the growing emphasis on integrity.

Nick Osborne, Vice President, Global Carbon and Environmental Products Trading at Shell“While momentum is undeniable, greater alignment and clearer guidance would help unlock the carbon market’s full potential.”

Insights into voluntary carbon market trends

The voluntary carbon market (VCM) is becoming a useful tool for helping companies work towards their net-zero goals. This research whitepaper explores what drives demand, how businesses choose and procure carbon credits, and why credibility and impact are critical to building effective carbon credit strategies.

Buyers navigating a fragmented market

Absent that alignment, existing differences in buyer priorities play out more starkly – shaping how quality is interpreted, risk is managed, and supply is secured in practice.

Shell’s PwC-commissioned research study3 shows just how varied these approaches are: some corporates pursue multi-year offtakes to secure long-term, high-quality supply, while others rely on short-term tactical purchases. Priorities also differ – from rigorous measurement, reporting and verification (MRV) and reputational assurance to affordability and flexibility.

This diversity reflects the market’s complexity. But without shared definitions of quality and consistent claims frameworks, it’s harder to compare credits and scale best practice. In a crowded kitchen, what’s missing is a shared recipe. Frameworks such as the Paris Agreement Crediting Mechanism (PACM) and ICVCM can help set it, but trust and liquidity will grow only through consistent application, robust MRV and more transparent data across registries.

Demand driving market quality

At the BNEF roundtable, buyers described carbon credits as “the mortar between the bricks” – playing a strategic role in decarbonisation plans and filling unavoidable gaps with credible, measurable outcomes.

That strategic role is reshaping demand. Buyers are becoming more discerning, seeking project‑level data, scrutinising developer track records and insisting on transparency around impact claims alongside price.

Market data suggests that this shift is starting to take hold. Sylvera’s Q1 2026 analysis shows that investment-grade (BBB+) credits are not only getting more expensive – averaging $20.10 in Q1 2026 versus $18.10 in Q1 2025 – but also taking a larger share of activity, accounting for nearly two-thirds of the total market value.4

These are encouraging signals. But sustaining them depends on confidence in future demand. Transparency and accountability are advancing – yet without clear, durable demand signals, developers cannot invest at the scale required to deliver high‑integrity supply.

Corporate demand as a catalyst

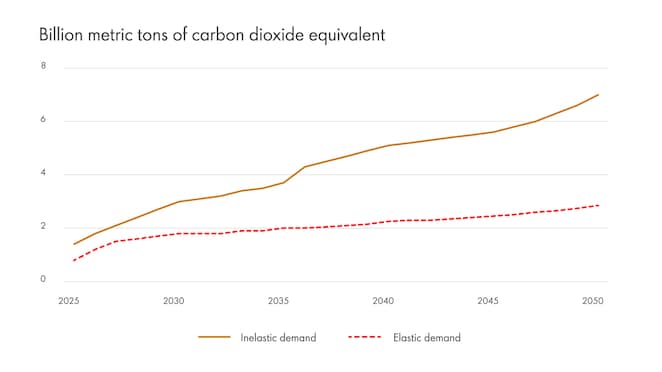

Corporate activity remains the main catalyst for market growth, with forecasts suggesting demand could reach almost seven billion tonnes of CO₂ by 2050.5 Early engagement – through forward purchases, long-term partnerships and investing in emerging technologies – sends powerful price and volume signals that can allow high-quality projects to scale.

Some corporates are already showing how this works, integrating credits into wider emissions-reduction strategies and balancing avoidance and removals based on cost, availability and credibility. Crucially, they treat credits not as a substitute for decarbonisation, but as a complement for residual emissions.

As buyer expectations for integrity and robust MRV continue to rise, they will drive the market toward higher standards – ensuring carbon credits remain a trusted and effective tool in the global decarbonisation journey.

Baseline long-term carbon credit demand scenarios

Peak corporate carbon credit demand in 2050:

6.9GtCO2e

Note: Inelastic demand scenario assumes companies will be obligated to achieve their sustainability goals regardless of the cost and any reputational risk. Elastic demand scenario assumes that companies will lessen their financial commitment to carbon credits as prices go up, and reputational risk.

Source: BloombergNEF5 for BNEF Summit London 2025

Finding harmony through complexity

Making the carbon market work increasingly comes down to a few essentials: consistent standards, better data and the capability to assess quality with confidence.

At Shell, our role is not only to buy and sell credits, but to help shape a trustworthy market. We engage with policymakers and market initiatives such as ICVCM and IETA to support high-integrity standards, and we apply our own due diligence to assess credit quality with confidence and increase transparency for corporate buyers.

A market taking shape

From the discussions at Shell’s BNEF roundtable, a picture is emerging. Integrity bodies are creating structure, buyers are raising expectations and data quality is improving.

The recipe for success is coming together – but it will only scale if buyers stay engaged. Acting early, backing high integrity projects, insisting on robust MRV and making credible claims are what will turn progress into lasting market depth.

It’s also important to recognise that definitions of “high quality” will continue to evolve. With better data, stronger standards and more market experience, the bar has risen materially in just a few years – a sign of progress.

The next phase for carbon markets won’t be defined by complexity, but by collaboration – and every good kitchen thrives on that.

Ready to include carbon credits into your decarbonisation strategy?

Get in touch with our experts to find out how Shell can help you purchase high-quality, credible carbon credits from projects that make a difference.

Date of publication: Jun, 2026

Shell Environmental Products

Used in addition to low-carbon fuels and decarbonisation technologies, quality carbon credits offer business leaders the choice to compensate for emissions that cannot yet be avoided or reduced.

Sources

1 Sylvera. “Compliance vs. Voluntary: How Carbon Credit Market Convergence Creates New Opportunities”. n.d.

2 MSCI. “Carbon Credits Come of Age in 2025”. January 6, 2026.

3 Shell Low Carbon Solutions. “Navigating the Voluntary Carbon Market (VCM): Insights into Buyer Behaviour, Barriers and Opportunities”. n.d.

4 Sylvera. “Q1 2026 Carbon Data Snapshot”. April 8, 2026.

Disclaimer

Disclaimer

*Carbon credits are not a substitute for switching to low-emission energy solutions or reducing the use of fossil fuels. Shell encourages their customers to focus first on emissions that can be avoided or reduced and only then compensate for the remaining emissions through the purchase and retirement of voluntary carbon credits. Where specific projects or project types generating carbon credits are referred to in this webpage, Shell does not guarantee that it has the carbon credits from these specific projects available in its current carbon credit portfolio; benefits of projects described are based on publicly available information from Project Developer Documents and/or provided by Project Developers. Shell does not guarantee projects will deliver the benefits exactly as described.

**Photos are for illustrative purposes only and may not depict the specific projects in Shell's current carbon credit portfolio.

Cautionary note

Cautionary note

The companies in which Shell plc directly and indirectly owns investments are separate legal entities. In this content “Shell”, “Shell Group” and “Group” are sometimes used for convenience to reference Shell plc and its subsidiaries in general. Likewise, the words “we”, “us” and “our” are also used to refer to Shell plc and its subsidiaries in general or to those who work for them. These terms are also used where no useful purpose is served by identifying the particular entity or entities. ‘‘Subsidiaries’’, “Shell subsidiaries” and “Shell companies” as used in this content refer to entities over which Shell plc either directly or indirectly has control. The terms “joint venture”, “joint operations”, “joint arrangements”, and “associates” may also be used to refer to a commercial arrangement in which Shell has a direct or indirect ownership interest with one or more parties. The term “Shell interest” is used for convenience to indicate the direct and/or indirect ownership interest held by Shell in an entity or unincorporated joint arrangement, after exclusion of all third-party interest.

Forward-Looking statements

This content contains forward-looking statements (within the meaning of the U.S. Private Securities Litigation Reform Act of 1995) concerning the financial condition, results of operations and businesses of Shell. All statements other than statements of historical fact are, or may be deemed to be, forward-looking statements. Forward-looking statements are statements of future expectations that are based on management’s current expectations and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in these statements. Forward-looking statements include, among other things, statements concerning the potential exposure of Shell to market risks and statements expressing management’s expectations, beliefs, estimates, forecasts, projections and assumptions. These forward-looking statements are identified by their use of terms and phrases such as “aim”; “ambition”; ‘‘anticipate’’; “aspire”, “aspiration”, ‘‘believe’’; “commit”; “commitment”; ‘‘could’’; “desire”; ‘‘estimate’’; ‘‘expect’’; ‘‘goals’’; ‘‘intend’’; ‘‘may’’; “milestones”; ‘‘objectives’’; ‘‘outlook’’; ‘‘plan’’; ‘‘probably’’; ‘‘project’’; ‘‘risks’’; “schedule”; ‘‘seek’’; ‘‘should’’; ‘‘target’’; “vision”; ‘‘will’’; “would” and similar terms and phrases. There are a number of factors that could affect the future operations of Shell and could cause those results to differ materially from those expressed in the forward-looking statements included in this content, including (without limitation): (a) price fluctuations in crude oil and natural gas; (b) changes in demand for Shell’s products; (c) currency fluctuations; (d) drilling and production results; (e) reserves estimates; (f) loss of market share and industry competition; (g) environmental and physical risks, including climate change; (h) risks associated with the identification of suitable potential acquisition properties and targets, and successful negotiation and completion of such transactions; (i) the risk of doing business in developing countries and countries subject to international sanctions; (j) legislative, judicial, fiscal and regulatory developments including tariffs and regulatory measures addressing climate change; (k) economic and financial market conditions in various countries and regions; (l) political risks, including the risks of expropriation and renegotiation of the terms of contracts with governmental entities, delays or advancements in the approval of projects and delays in the reimbursement for shared costs; (m) risks associated with the impact of pandemics, regional conflicts, such as the Russia-Ukraine war and the conflict in the Middle East, and a significant cyber security, data privacy or IT incident; (n) the pace of the energy transition; and (o) changes in trading conditions. No assurance is provided that future dividend payments will match or exceed previous dividend payments. All forward-looking statements contained in this content are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Readers should not place undue reliance on forward-looking statements. Additional risk factors that may affect future results are contained in Shell plc’s Form 20-F for the year ended December 31, 2025 (available at www.shell.com/investors/news-and-filings/sec-filings.html and www.sec.gov). These risk factors also expressly qualify all forward-looking statements contained in this content and should be considered by the reader. Each forward-looking statement speaks only as of the date of this content. Neither Shell plc nor any of its subsidiaries undertake any obligation to publicly update or revise any forward-looking statement as a result of new information, future events or other information. In light of these risks, results could differ materially from those stated, implied or inferred from the forward-looking statements contained in this content.

Shell’s net carbon intensity

Also, in this content we may refer to Shell’s “net carbon intensity” (NCI), which includes Shell’s carbon emissions from the production of our energy products, our suppliers’ carbon emissions in supplying energy for that production and our customers’ carbon emissions associated with their use of the energy products we sell. Shell’s NCI also includes the emissions associated with the production and use of energy products produced by others which Shell purchases for resale. Shell only controls its own emissions. The use of the terms Shell’s “net carbon intensity” or NCI is for convenience only and not intended to suggest these emissions are those of Shell plc or its subsidiaries.

Shell’s net-zero emissions target

Shell’s operating plan and outlook are forecasted for a three-year period and ten-year period, respectively, and are updated every year. They reflect the current economic environment and what we can reasonably expect to see over the next three and ten years. Accordingly, the outlook reflects our combined Scope 1 and 2 target, NCI target and our oil products ambition over the next ten years. However, Shell’s operating plan and outlook cannot reflect our 2050 net-zero emissions target, as this target is outside our planning period. Such future operating plans and outlooks could include changes to our portfolio, efficiency improvements and the use of carbon capture and storage and carbon credits. In the future, as society moves towards net-zero emissions, we expect Shell’s operating plans and outlooks to reflect this movement. However, if society is not net zero in 2050, as of today, there would be significant risk that Shell may not meet this target.

Forward-Looking non-GAAP measures

This content may contain certain forward-looking non-GAAP measures such as free cash flow and underlying operating expenses. We are unable to provide a reconciliation of these forward-looking non-GAAP measures to the most comparable GAAP financial measures because certain information needed to reconcile those non-GAAP measures to the most comparable GAAP financial measures is dependent on future events some of which are outside the control of Shell, such as oil and gas prices, interest rates and exchange rates. Moreover, estimating such GAAP measures with the required precision necessary to provide a meaningful reconciliation is extremely difficult and could not be accomplished without unreasonable effort. Non-GAAP measures in respect of future periods which cannot be reconciled to the most comparable GAAP financial measure are calculated in a manner which is consistent with the accounting policies applied in Shell plc’s consolidated financial statements.

The contents of websites referred to in this content do not form part of this content.

We may have used certain terms, such as resources, in this content that the United States Securities and Exchange Commission (SEC) strictly prohibits us from including in our filings with the SEC. Investors are urged to consider closely the disclosure in our Form 20-F, File No 1-32575, available on the SEC website www.sec.gov.